Family budget travel planning is the process of setting a firm spending limit, dividing funds across key categories, and tracking every dollar so your family vacation stays affordable and stress-free. Most families skip the budget cap and pick the destination first. That single mistake is the leading cause of vacation debt. The right approach, as outlined by Finhabits and Cathy Kessel's Family Travel Budget Planning System, starts with what you can realistically afford, then builds the trip around that number. Done well, a travel budget keeps your spending intentional, eliminates financial surprises, and lets you focus on making memories instead of watching your bank account.

How does family budget travel planning actually work?

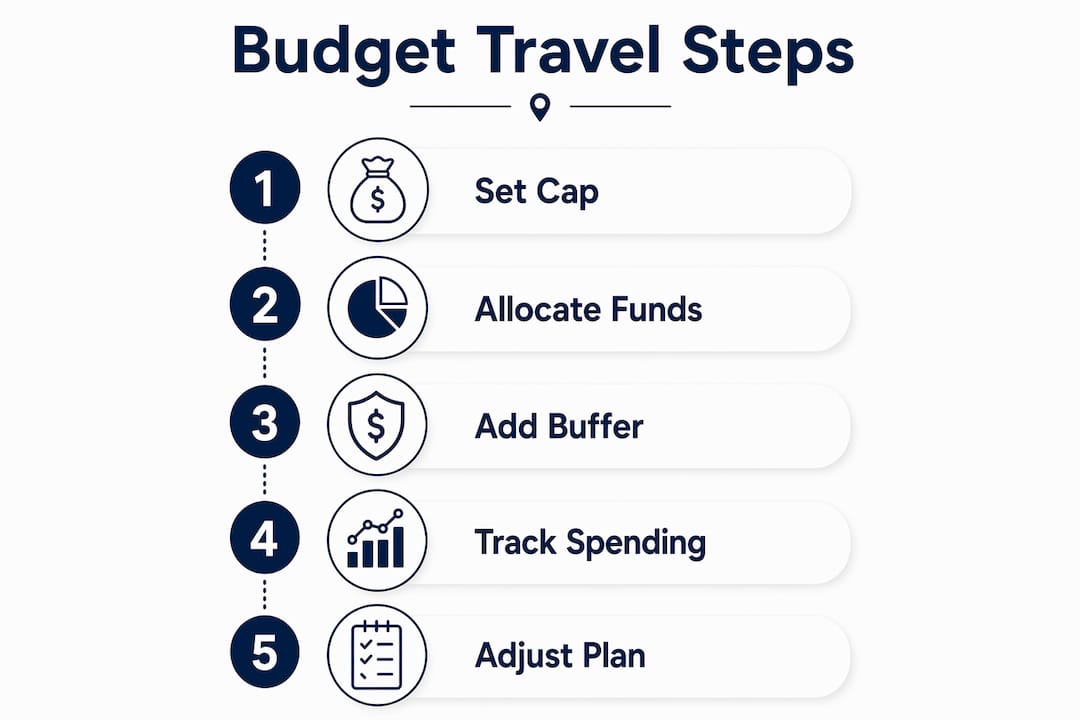

Family budget travel planning works by establishing a spending ceiling before you research any destination. Finhabits advises starting with the number, not the destination, and building every decision from there. This single shift prevents wishful thinking from driving your choices.

Once you have a ceiling, divide the total across five core categories:

- Transportation (flights, gas, car rental, or train tickets)

- Lodging (hotels, vacation rentals, hostels, or campgrounds)

- Food (restaurants, groceries, and snacks)

- Activities (entrance fees, tours, and entertainment)

- Hidden costs (luggage fees, mobile data, tips, and souvenirs)

A rough guideline: use 10% of your household net income as the upper ceiling for a single trip. That figure keeps the vacation from competing with your mortgage or emergency fund.

UMB's budgeting guidance recommends adding a contingency buffer of 10–20% on top of your estimated total. Unplanned fees like parking, baggage charges, and urgent medical visits appear on almost every family trip. Keep this buffer as a separate line item. It is not discretionary spending. It exists only for genuine surprises.

Pro Tip: Write your budget cap on paper or in a shared document before you open a single travel website. Seeing the number first stops destination envy from inflating your plans.

Small, high-frequency costs are the category most families underestimate. UMB highlights that smaller daily expenses, not one large missed payment, cause most budget overruns. Budget explicitly for daily meals, local transit, and tips. These costs compound fast across a week-long trip with four or more people.

How to save up for your family trip efficiently

The most reliable way to fund a family vacation is to divide the total cost by the number of weeks until departure, then transfer that amount automatically each week. Finhabits recommends automating weekly transfers to a dedicated vacation savings account. Automation removes the temptation to redirect that money toward everyday expenses.

Here is a simple four-step savings system:

- Set your total budget cap. Include all five categories plus the contingency buffer.

- Open a dedicated savings account. Keep vacation funds completely separate from your checking account.

- Calculate your weekly savings target. Divide the remaining balance by weeks until departure.

- Automate the transfer. Schedule it for payday so the money moves before you spend it.

SaveToRoam's family holiday budget template adds one more layer: track paid amounts versus remaining costs, then recalculate your weekly target based on the remaining balance, not the original total. If you pay for flights early, your weekly savings target drops. This prevents you from over-saving and frees up cash for other needs.

Pro Tip: Label your vacation savings account with the destination name, such as "Colorado 2026." A named account makes the goal feel real and reduces the urge to dip into it.

Cutting unnecessary spending to fund the trip works better when you treat it as a short-term trade. Cancel one streaming service for three months. Pack lunch twice a week. Redirect those small amounts directly into the vacation account. The total adds up faster than most families expect.

What are the best ways to save on transportation and lodging?

Timing and flexibility are the two biggest levers for cutting transportation and lodging costs. NerdWallet states that travel prices fluctuate with demand, and early planning combined with reward points reduces expenses significantly. Booking flights and hotels three to six months in advance consistently yields lower rates than last-minute purchases.

Key cost-saving strategies for transportation and lodging:

- Travel off-peak or during shoulder season. Rates drop sharply outside school holiday windows. Late august and early september offer lower prices than peak summer weeks.

- Compare transportation modes. For trips under 500 miles, driving often costs less than flying once you factor in baggage fees and airport transfers.

- Use fare comparison tools. Google Flights, Kayak, and Hopper let you track price trends and set alerts for drops.

- Redeem reward points. Credit card travel rewards and airline miles can cover flights or hotel nights entirely.

- Choose budget-friendly lodging. Vacation rentals through Vrbo or Airbnb often cost less per night than hotels for families of four or more, and they include kitchens that cut food costs.

- Stay flexible with dates. Shifting your departure by two or three days can reduce flight costs by a meaningful amount.

Camping and state park lodging represent the most affordable option for families comfortable with outdoor travel. National Park Service campgrounds across the United States charge a fraction of hotel rates and deliver experiences that kids remember for years.

How do you track spending during a family trip?

Real-time expense tracking prevents small overruns from becoming large ones. Cathy Kessel's Family Travel Budget Planning System recommends daily check-ins where you compare planned spending against actual spending, then adjust the next day's budget accordingly. A five-minute review each evening is enough to stay in control.

Practical tracking habits that work on the road:

- Use a free expense tracking app like Trail Wallet or a shared Google Sheet to log every purchase.

- Check your running total each evening before bed.

- Adjust the next day's food or activity budget if you overspent the day before.

- Track hidden costs separately: parking, resort fees, and mobile data charges add up fast.

- Pack snacks, sunscreen, and basic medications before you leave. Last-minute airport or resort purchases cost two to three times the normal price.

Pro Tip: Assign one adult the role of "budget keeper" for the trip. One person logging expenses is more consistent than two people assuming the other is tracking.

Keep the contingency buffer as a completely separate line in your tracker. UMB's guidance is clear: the buffer covers genuine surprises, not upgrades or impulse purchases. If you finish the trip without touching it, that money goes back into savings.

What are the most common family travel budget mistakes?

Most budget failures follow a predictable pattern. Recognizing these mistakes before your trip is the fastest way to avoid them.

- Choosing the destination before setting the budget. This is the single most common error. Picking a destination first leads to reverse-engineering a budget that fits the dream, not the reality.

- Ignoring small daily costs. Coffee, snacks, tips, and local transit feel minor individually. Across seven days for a family of four, they can add hundreds of dollars to your total.

- Waiting until after the trip to review spending. Cathy Kessel notes that overspending happens most when plans are rushed or unclear. Reviewing only after the trip removes your ability to course-correct.

- Using the contingency buffer as upgrade money. The buffer is not a bonus. Treating it as permission to spend more erases the financial safety net it was designed to provide.

- Rushing bookings. Last-minute flights, hotels, and tours consistently cost more and offer fewer options. Rushed decisions also increase the chance of choosing poorly rated accommodations.

- Failing to update the budget as the trip evolves. Prices change. Plans shift. A budget that is not updated becomes inaccurate and loses its value as a decision-making tool.

Key Takeaways

Effective family budget travel planning requires setting a firm spending cap first, allocating funds across all categories including hidden costs, and tracking expenses daily to stay in control throughout the trip.

| Point | Details |

|---|---|

| Set the cap before the destination | Choose what you can afford first, then pick a trip that fits that number. |

| Include a contingency buffer | Add 10–20% on top of estimated costs and keep it as a separate budget line. |

| Automate your savings | Divide the total by weeks until departure and transfer that amount automatically each week. |

| Track spending daily | Compare planned versus actual costs each evening and adjust the next day's budget. |

| Watch small daily costs | Meals, tips, and local transit cause more overruns than any single large expense. |

Why I think most families budget travel backwards

Most travel budgeting advice focuses on tactics: use points, book early, eat at local spots. That advice is solid. But the families I see struggle most are not missing tactics. They are missing a firm number written down before any planning begins.

The moment you open a travel website without a cap, you are negotiating against yourself. Every beautiful resort photo raises your mental anchor. By the time you sit down to budget, you are already rationalizing a number that is too high.

What changed my own approach was treating the budget as a living document, not a one-time spreadsheet. Reviewing it before booking, during the trip, and after return turns it into a decision-making tool rather than a guilt record. That shift is the difference between a trip that leaves you refreshed and one that leaves you anxious about your credit card statement.

The other thing most articles skip: the contingency buffer is not pessimism. It is confidence. Knowing you have 15% set aside for surprises means a flat tire or a sick kid does not derail the whole trip emotionally. You handle it, you move on, and you still enjoy the vacation.

Budgeting for a family trip is not about limiting fun. It is about protecting it.

— Dom

Planytera makes family trip planning faster and less stressful

Planning a family trip on a budget means juggling dozens of decisions at once: flights, lodging, activities, dietary needs, and daily costs. That coordination takes hours when done manually.

Planytera handles the heavy lifting with AI-powered, personalized itineraries built around your budget cap, pace, and family preferences. You set the parameters, and Planytera generates a tailored day-by-day plan in moments. You can adjust any part of the itinerary on the fly as plans change. The platform also works offline, so your plan is accessible even without a data connection. Families can start planning their trip at Planytera and see sample itineraries to understand exactly how the planning process works before committing.

FAQ

What is family budget travel planning?

Family budget travel planning is the process of setting a realistic spending cap, dividing it across categories like transportation, lodging, food, and activities, and tracking expenses throughout the trip to avoid overspending.

How much should a family budget for a vacation?

A practical guideline is to use no more than 10% of your household net income as the ceiling for a single trip. Add a contingency buffer of 10–20% on top of your estimated costs to cover unexpected expenses.

When should you start saving for a family vacation?

Start saving as soon as you set your budget cap. Divide the total cost by the number of weeks until departure and automate a weekly transfer to a dedicated vacation savings account.

What costs do families most often forget to budget for?

Small, high-frequency costs like daily meals, local transit, tips, parking, and mobile data are the most commonly overlooked. These expenses compound quickly across a multi-day trip and cause more overruns than any single large purchase.

How do you stay on budget during a family trip?

Do a five-minute expense check each evening, comparing planned spending against actual spending. Adjust the next day's budget based on your current status, and keep your contingency buffer as a separate line that covers only genuine surprises.